By publicly extending an olive branch to American investors, Iranian officials maybe testing Washington’s appetite for a broader détente—one that moves beyond nuclear containment toward economic normalization. Whether this message reflects a genuine shift or strategic posturing, and whether it leads to meaningful progress, will likely depend on what both sides are prepared to offer in talks that began in Oman on April 12.

However, a wide array of US sanctions, combined with deeply unfavorable conditions inside Iran, would make investment by the US—or any developed country—extremely difficult.

A bigger deal than 2015?

Recent comments by President Masoud Pezeshkian and Foreign Minister Abbas Araghchi suggest that Iran is seeking more than relief from secondary US sanctions—reimposed after Washington’s 2018 exit from the JCPOA—and is also pushing for the removal of primary sanctions that have long restricted American trade and investment in Iran.

In May 2018, President Donald Trump unilaterally withdrew the United States from the JCPOA nuclear agreement between Iran and world powers and reimposed the secondary US sanctions that had been lifted under the deal. These sanctions aim to penalize any third parties breaking US restrictions on Iran.

Under current conditions, with both primary and secondary sanctions in place, no US company or individual is permitted to invest in Iran. Any such investment would only be possible after a nuclear agreement is reached and Iran begins implementing its commitments. Washington is unlikely to lift all sanctions upfront without Tehran first dismantling at least part of its uranium enrichment infrastructure and reducing or transferring its stockpile of highly enriched uranium.

What Iranian officials said about US investment

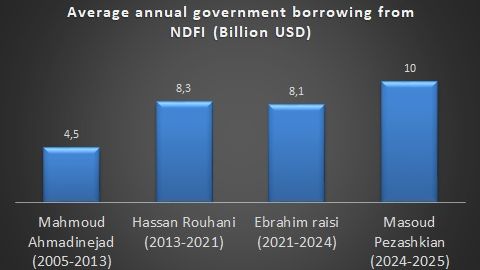

In October, President Pezeshkian said Iran needs at least $100 billion in foreign investment to reach an annual economic growth rate of eight percent. He emphasized that improving foreign relations is key to attracting such investment. Iran has averaged less than 3% annual growth throughout the 46 years of clerical government.

In a more pointed message this week, Pezeshkian said that Supreme Leader Ali Khamenei has “no objection to American investors” entering the Iranian market. “Let them come and invest,” he said. “But we oppose plotting, regime change efforts, and destructive policies. Iran is not a place for conspiracies or espionage followed by assassinations. [All] investors are welcome to invest in our country.”

Foreign Minister Abbas Araghchi reinforced this line in a Washington Post op-ed, arguing that the onus is on Washington to allow American companies to tap into what he described as a “trillion-dollar opportunity” in Iran, though he did not offer specifics.

While Khamenei has not commented on the talks or investment prospects, as Iran’s top decision-maker on foreign policy, he has authorized indirect negotiations with Washington and is expected to be closely involved in determining their scope and terms.

What type of US sanctions on Iran are in place?

After the 2015 nuclear deal the US lifted most of nuclear-related secondary sanctions. However, the primary US sanctions—which date back as far as the 1980s and ban nearly all trade and financial dealings between US persons and Iran—remained in force even after the deal.

These sanctions made it virtually impossible for American companies to invest in or trade with Iran, even during the brief JCPOA implementation period, unless they obtained special licenses from the US Treasury’s Office of Foreign Assets Control (OFAC).

For instance, Boeing was able to sign an agreement with Iran in 2016 to sell commercial aircraft after receiving a special OFAC license under the Obama administration. The company could not have even provided maintenance services without such an exemption under regulations like the Iranian Transactions Regulations (ITR).

Much to the dismay of Iran, Boeing’s aircraft were never delivered, and the license was revoked after the Trump administration exited the JCPOA.

Similar restrictions under the Export Administration Regulations (EAR), enforced by the US Commerce Department, also prevented non-US companies like Airbus from selling aircraft to Iran if they contained more than 10 percent US-origin components—unless licensed by OFAC.

Domestic impediments to investments

Beyond sanctions, one of the most significant barriers to American and broader international investment in Iran is the structure of its state-controlled economy. The system is riddled with opaque regulations, inconsistent enforcement, and non-transparent business practices. Key sectors are dominated by economic conglomerates affiliated with Supreme Leader Ali Khamenei and the Islamic Revolutionary Guard Corps (IRGC), creating an uneven playing field and discouraging foreign entrants.

Iran’s economy is effectively closed, especially when it comes to consumer-facing industries. Even domestic investors face serious risks due to unclear rules, political interference, and limited legal protections. While foreign companies can occasionally secure contracts for state-backed infrastructure projects—such as revamping oil and gas facilities—these are tightly controlled by government-linked entities and offer little access to Iran’s broader market. This model does not allow for the kind of real, diversified investment that would benefit Iran’s private sector or broader population.

A nuclear agreement, while potentially reducing the immediate risk of conflict and unlocking limited economic engagement, is not enough to attract serious Western investment. For that to happen, Iran would need to implement deeper reforms. This includes recalibrating its foreign policy, scaling back the IRGC’s grip on the economy, and creating a more transparent and rules-based business environment. Without such changes, the prospect of meaningful, long-term foreign investment will remain remote.